Hurricane Beryl: Impact on 2024 Atlantic Hurricane Season

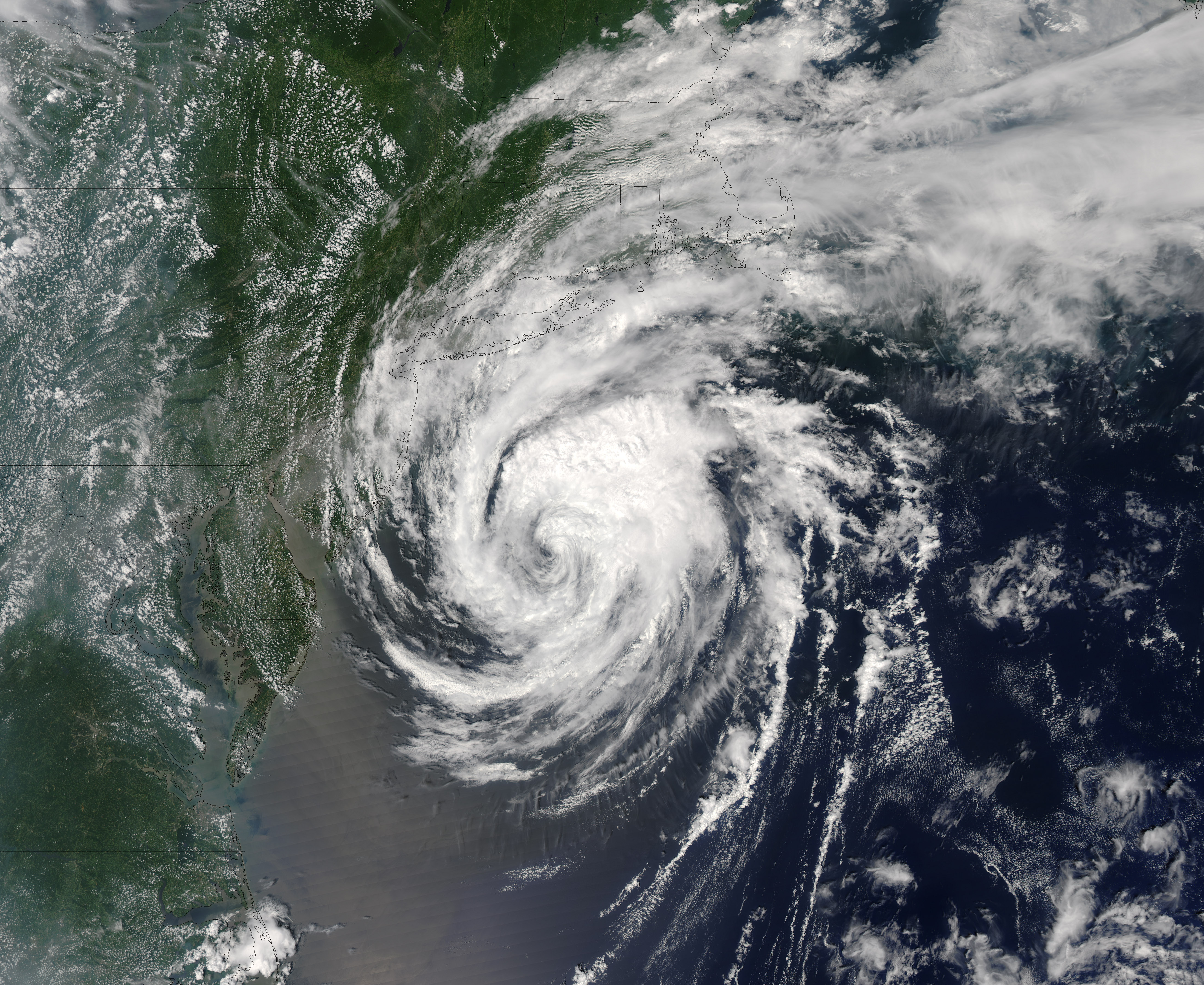

Hurricane Beryl’s rapid transformation from a tropical storm to a Category 5 hurricane has raised alarms for the 2024 Atlantic Hurricane season, which is already anticipated to be notably severe. Meteorologist Dr. Philip Klotzbach has pointed out that such early-season storm activity is unprecedented, eclipsing records from the historically active years of 1933 and 2005. The intense escalation of Hurricane Beryl, driven by above-average sea surface temperatures, underscores the growing unpredictability of tropical storms and their potential impacts on communities. As Beryl made landfall as a Category 1 hurricane near Matagorda, Texas, it unleashed devastating flooding and wind damage, highlighting the importance of climate-related insurance and flood damage coverage for homeowners in vulnerable areas. With millions left without power and facing an oppressive heatwave, the urgency for comprehensive disaster preparedness and insurance awareness has never been clearer in the face of such catastrophic weather events.

The recent emergence of Hurricane Beryl exemplifies the escalating threats posed by severe weather patterns as we enter the 2024 Atlantic Hurricane season. This storm’s swift upgrade to a Category 5 classification signals a concerning trend in tropical cyclone behavior, where storms intensify more rapidly, leaving little time for affected populations to respond. The implications of such storms extend beyond immediate destruction; they also raise significant questions regarding insurance coverage for flood damage and climate-related risks. As the aftermath of Beryl demonstrates, understanding the nuances of homeowners insurance, particularly in relation to natural disasters, is crucial for mitigating financial loss. As we brace for what could be an exceptionally intense hurricane season, the need for robust insurance solutions to address these evolving challenges becomes all the more pressing.

Hurricane Beryl and Its Impact on the 2024 Atlantic Hurricane Season

Hurricane Beryl’s rapid transformation from a tropical storm to a Category 5 hurricane is a stark warning for the upcoming 2024 Atlantic Hurricane season, which is anticipated to be more intense than average. According to Dr. Philip Klotzbach, a prominent research scientist at Colorado State University, the early emergence of such powerful storms is reminiscent of historic seasons renowned for their ferocity, particularly 1933 and 2005. With alarming sea surface temperatures contributing to Beryl’s swift escalation, the implications for coastal communities are severe, as a hurricane that intensifies quickly can catch residents off guard, reducing their preparation time and increasing the potential for catastrophic damage.

The rapid intensification of Hurricane Beryl underscores the urgent need for enhanced disaster preparedness and response strategies. As the storm made landfall in Texas, it wreaked havoc, causing flooding and uprooting trees, effectively transforming roads into rivers. The aftermath of such storms not only disrupts lives but also raises critical questions about the adequacy of existing flood damage coverage in homeowners’ insurance policies. With over 90% of homeowners lacking adequate flood insurance, the financial ramifications of such disasters can be devastating, leaving many to confront overwhelming repair costs without the necessary protection.

The Role of Climate-Related Insurance in Mitigating Hurricane Damage

With the increasing frequency of hurricanes like Beryl, the importance of climate-related insurance becomes more pronounced. Dale Porfilio, Chief Insurance Officer at Triple-I, emphasizes that while many homeowners are covered for typical damages, they often overlook the nuances of disaster preparedness, particularly when it comes to flood damage coverage. This oversight can lead to significant gaps in protection, especially in regions that are increasingly vulnerable to severe weather events. As climate change continues to exacerbate storm intensity and frequency, understanding the limitations of standard homeowners insurance is crucial for homeowners.

Moreover, the structural integrity of homes is tested during extreme weather conditions, and Porfilio warns that roofs designed to last for 20 years may succumb to the stresses of heat and wind, leading to premature damage. This highlights the necessity for homeowners to re-evaluate their insurance policies, ensuring they include adequate provisions for roof damage alongside flood coverage. As the 2024 Atlantic Hurricane season approaches, homeowners should take proactive measures to align their insurance policies with the evolving climate risks, thus safeguarding their properties against future hurricanes.

Flood Damage Coverage: A Critical Insurance Gap for Homeowners

Flood damage coverage remains one of the most significant insurance gaps in the United States, with an alarming statistic revealing that over 90% of homeowners do not have sufficient flood protection. This lack of awareness can prove detrimental, especially in the wake of hurricanes like Beryl, which expose the vulnerabilities of properties to water damage. Homeowners often mistakenly believe that their standard insurance policies cover flooding, leading to a false sense of security that can result in devastating financial losses when disaster strikes.

Addressing this gap in flood damage coverage is vital, particularly as climate-related events become more prevalent. Insurance experts advocate for increased education and awareness among homeowners regarding the specifics of their policies. By understanding the limitations of traditional coverage and the necessity for additional flood insurance, property owners can better prepare for the impacts of severe storms. As the 2024 Atlantic Hurricane season approaches, it is imperative for homeowners to take action, ensuring they are equipped with the right insurance to withstand potential disasters.

The Financial Implications of the 2024 Atlantic Hurricane Season

As the 2024 Atlantic Hurricane season looms, the insurance industry braces itself for potential financial repercussions stemming from predicted above-average storm activity. Triple-I CEO Sean Kevelighan points out that the property and casualty market is prepared for such challenges, maintaining a surplus of $1.1 trillion to honor policy commitments. However, the interplay of climate-related trends, inflation, and legal system abuses poses significant obstacles for insurers, complicating their ability to effectively manage risks associated with hurricanes like Beryl.

The financial landscape for homeowners is also affected by these trends, as rising costs related to storm damage can drive up insurance premiums. In states like Florida, where a significant portion of homeowners insurance litigation occurs, the pressure on insurers is even more pronounced. Legislative reforms have begun to address some of these issues, but the ongoing challenges highlight the need for homeowners to be proactive in understanding their coverage options. As the 2024 season approaches, the financial implications for both the insurance industry and homeowners underscore the critical importance of preparedness and comprehensive insurance policies.

The Importance of Preparedness in the Face of Hurricane Threats

In light of Hurricane Beryl’s rapid intensification, the importance of preparedness cannot be overstated. Quick-response strategies, including evacuation plans and emergency kits, should be a priority for residents in hurricane-prone areas. The unpredictable nature of storms means that communities must be equipped to react swiftly, as demonstrated by the chaos that ensued during Beryl’s landfall in Texas. By fostering a culture of preparedness, homeowners can significantly mitigate the risks associated with hurricanes and safeguard their families and properties.

Furthermore, local governments play a crucial role in enhancing community readiness. Investments in infrastructure improvements, such as better drainage systems and storm shelters, can help reduce the impact of flooding and storm damage. Public awareness campaigns about the realities of climate-related insurance and the need for adequate flood coverage can empower homeowners to take charge of their safety. As the 2024 Atlantic Hurricane season approaches, reinforcing preparedness measures will be vital in minimizing the potential devastation caused by hurricanes like Beryl.

Understanding the Risks Associated with Tropical Storms and Hurricanes

Tropical storms and hurricanes present a unique set of risks that can escalate rapidly, as evidenced by Hurricane Beryl’s swift transition from a tropical storm to a Category 5 hurricane. Understanding these risks is essential for residents living in coastal areas who are often in the path of such storms. With the Atlantic Ocean’s rising temperatures contributing to storm intensification, the likelihood of encountering severe weather events increases, making education about these phenomena critical for effective disaster planning.

Moreover, the impacts of tropical storms extend beyond immediate wind damage; they also include heavy rainfall and resultant flooding, which can wreak havoc on infrastructure and homes. Homeowners must be aware of the multifaceted nature of these storms to adequately prepare their properties and families. Investing in proper insurance coverage, including flood insurance, is a key component of risk management that can help alleviate the financial burdens associated with storm damage. As we approach the 2024 Atlantic Hurricane season, a comprehensive understanding of these risks is paramount to ensuring community resilience.

The Role of Insurers in Preparing for Hurricane Season

Insurance companies are increasingly recognizing their pivotal role in preparing for the hurricane season, particularly with the anticipated challenges posed by the 2024 Atlantic Hurricane season. Sean Kevelighan, CEO of Triple-I, emphasizes the necessity for insurers to maintain robust capital reserves to meet policyholder claims following major storms like Beryl. This preparation involves not only financial readiness but also a commitment to educating homeowners about their coverage options and the importance of including flood damage protection in their policies.

Additionally, insurers are adapting to the changing landscape of climate risks by enhancing their risk modeling capabilities. As the frequency of intense storms rises, understanding the specific vulnerabilities of different regions becomes increasingly crucial. This proactive approach allows insurers to price their products more accurately and ensure that they can adequately support their policyholders in times of crisis. As the 2024 season approaches, the collaboration between insurers and communities in preparing for hurricanes will be essential to minimizing the human and economic toll of these disasters.

Legal and Regulatory Challenges in the Insurance Industry

The insurance industry faces a myriad of legal and regulatory challenges, particularly in states like Florida, where over 70% of homeowners insurance litigation occurs. These challenges can significantly impact insurers’ ability to respond effectively to claims following hurricanes like Beryl. As legal disputes can delay payouts and complicate the claims process, it is crucial for both insurers and homeowners to navigate these complexities to ensure a smoother recovery following storm events.

Furthermore, regulatory constraints in states such as California have hindered insurers’ abilities to adapt to inflationary pressures and the rising costs associated with climate-related risks. Insurers must balance the need for profitability with the demand for affordable coverage, which can be particularly challenging in high-risk areas. As the 2024 Atlantic Hurricane season approaches, addressing these legal and regulatory issues will be essential for fostering a resilient insurance market that can effectively support homeowners in times of crisis.

The Future of Hurricane Preparedness in a Changing Climate

As climate change continues to alter the landscape of hurricane activity, the future of hurricane preparedness must evolve to keep pace with these changes. The rapid escalation of storms like Hurricane Beryl serves as a reminder that residents and authorities alike need to adapt their strategies to mitigate the impacts of increasingly intense hurricanes. This includes not only improving infrastructure and emergency response systems but also enhancing public awareness regarding the importance of insurance coverage and disaster preparedness.

In addition, community resilience initiatives must prioritize education about climate risks and the importance of comprehensive insurance policies. By fostering a culture of preparedness and encouraging proactive measures, communities can better navigate the challenges posed by future hurricanes. As we look ahead to the 2024 Atlantic Hurricane season and beyond, it is imperative to embrace innovative approaches to hurricane preparedness that account for the evolving nature of climate-related threats.

Frequently Asked Questions

What caused Hurricane Beryl to escalate to a Category 5 hurricane during the 2024 Atlantic Hurricane season?

Hurricane Beryl rapidly escalated to a Category 5 hurricane due to significantly above-average sea surface temperatures. This rapid intensification poses serious risks as it allows less time for communities to prepare and evacuate, highlighting the growing concerns for the 2024 Atlantic Hurricane season.

How does Hurricane Beryl’s impact compare to past hurricanes in the 2024 Atlantic Hurricane season?

Hurricane Beryl’s swift transition from a tropical storm to a Category 5 hurricane is reminiscent of the extreme storm activity seen in the busy 1933 and 2005 hurricane seasons. This trend indicates that the 2024 Atlantic Hurricane season could be one of above-average intensity, raising alarms for potential flood damage and other impacts.

What type of insurance should homeowners consider after Hurricane Beryl’s landfall?

Homeowners should evaluate their climate-related insurance, particularly focusing on flood damage coverage. Hurricane Beryl’s landfall highlighted that over 90% of homeowners lack adequate flood coverage, which is crucial as standard homeowners insurance typically does not include flood damage.

What were the consequences of Hurricane Beryl’s flooding in Texas?

Hurricane Beryl caused significant flooding in Texas, transforming roads into rivers and disrupting power lines. The aftermath of the storm led to widespread power outages, with restoration expected to take days or even weeks, which is particularly dangerous during a sweltering heatwave.

What lessons can be learned from Hurricane Beryl regarding homeowners insurance?

Hurricane Beryl serves as a reminder for homeowners to review their insurance policies, particularly regarding flood damage coverage. Many mistakenly believe their homeowners insurance covers flooding, but this is often not the case. After the storm, it’s essential to ensure that your policy includes adequate protection against such risks.

How does Hurricane Beryl illustrate the broader trends affecting the insurance industry?

Hurricane Beryl underscores the growing challenges faced by the insurance industry in light of climate-related events. The predicted well above-average 2024 Atlantic Hurricane season is prompting insurers to maintain sufficient capital for claims, while also navigating issues such as legal system abuse and regulatory constraints that impact their operational costs.

What are the implications of Hurricane Beryl for future hurricane preparedness?

The rapid intensification seen with Hurricane Beryl suggests that future hurricanes may escalate quickly, reinforcing the need for better preparedness measures. Communities should prioritize timely evacuations and ensure they have the necessary climate-related insurance to mitigate potential flood damage.

| Key Point | Details |

|---|---|

| Hurricane Beryl’s Rapid Escalation | Beryl escalated from a tropical storm to a Category 5 hurricane, indicating a concerning trend for the 2024 Atlantic hurricane season. |

| Record Early Season Activity | This early-season storm activity has broken records set in 1933 and 2005, highlighting an alarming increase in hurricane intensity. |

| Impact of Sea Surface Temperatures | Above-average sea surface temperatures contributed to Beryl’s rapid intensification, making storms more dangerous with less preparation time for affected populations. |

| Landfall and Damage | Hurricane Beryl made landfall in Matagorda, Texas, as a Category 1 hurricane, causing significant flooding and power outages. |

| Insurance Implications | The hurricane’s impact raises concerns about flood coverage gaps, with over 90% of homeowners lacking adequate flood insurance. |

| Regulatory Challenges | The insurance industry faces challenges from legal abuses, regulatory environments, and inflation that impact loss costs. |

| California’s Insurance Market | California’s Proposition 103 complicates insurers’ ability to manage wildfire-related risks and inflation. |

Summary

Hurricane Beryl’s rapid escalation from a tropical storm to a Category 5 hurricane highlights significant concerns for the upcoming 2024 Atlantic hurricane season. The early activity and intensity of Beryl, along with its consequences, underscore the need for improved preparedness and insurance coverage against natural disasters. As climate change continues to influence weather patterns, understanding the implications for property insurance, particularly flood coverage, has never been more crucial.