Georgia Insurance Affordability: Rising Costs and Risks

Georgia insurance affordability is a growing concern as rising claim frequency and increasing insurer costs threaten the financial well-being of its residents. According to a recent issue brief by the Insurance Information Institute, the state’s below-average income juxtaposed with above-average insurance expenditures has led to Georgia ranking 42nd for affordable homeowners insurance and a staggering 47th for personal auto affordability. With skyrocketing litigation costs compounding the problem, many Georgians are grappling with the reality of higher insurance costs. The implications of these trends not only affect individual policyholders but also pose significant risks to the overall economic landscape of the state. As we delve deeper into the factors influencing insurance costs in Georgia, including the impact of tort reform and climate-related disasters, it becomes clear that action is necessary to restore affordability.

The issue of insurance affordability in Georgia encompasses a range of challenges that residents face when securing coverage for their homes and vehicles. With a notable disparity between income levels and insurance expenses, many individuals find themselves burdened by steep premiums. Additionally, the state’s legal landscape contributes to escalating costs, as litigation related to claims has surged in recent years. As we explore this topic further, it’s essential to examine the various elements at play, including the influence of homeowners insurance rates, the prevalence of underinsured motorists, and the role of proposed tort reform measures aimed at alleviating some of these financial pressures. Understanding these interconnected factors is crucial for Georgians seeking to navigate the complexities of insurance affordability.

Understanding Georgia Insurance Affordability

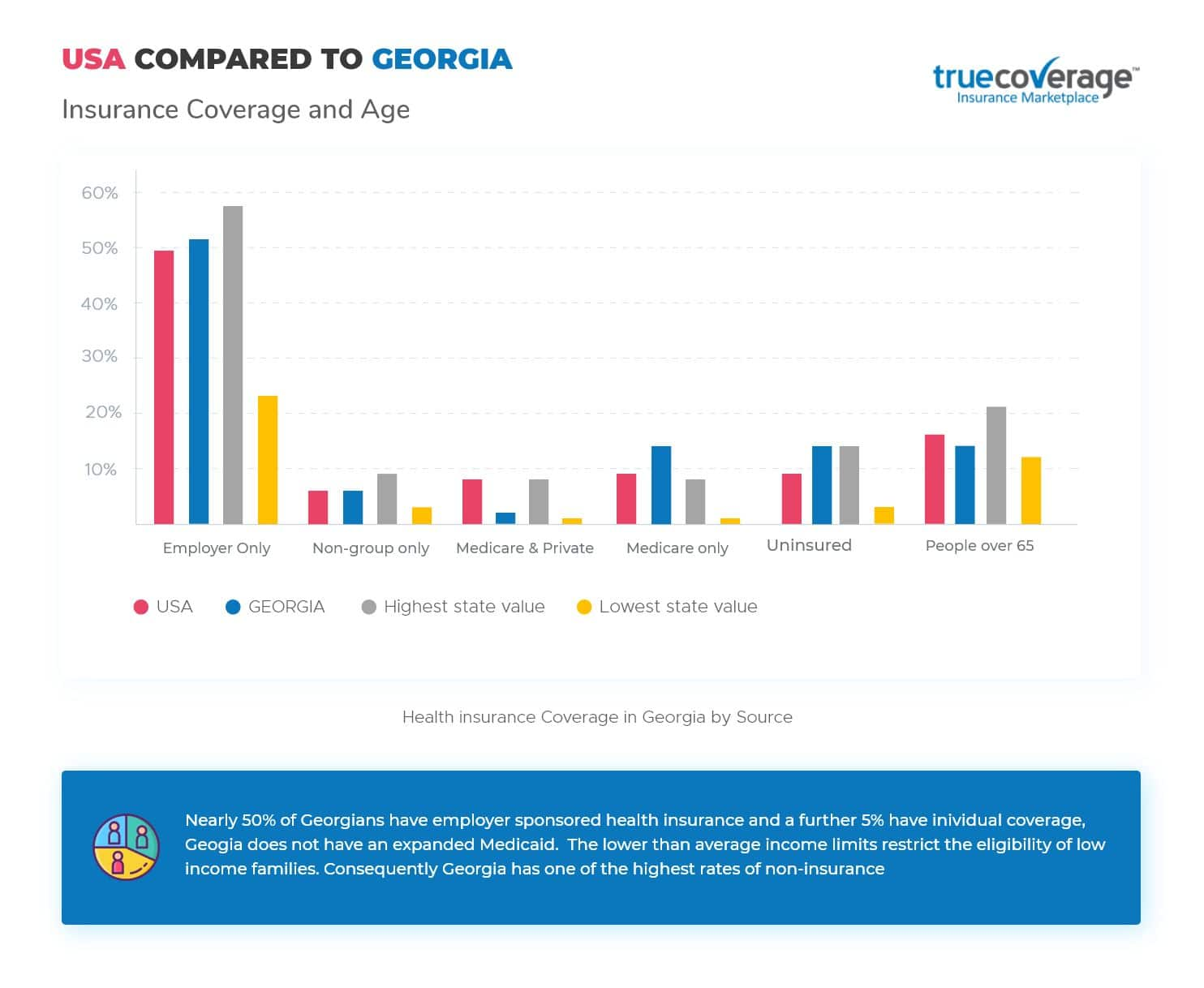

Insurance affordability in Georgia has become a pressing concern as various factors contribute to increased costs and reduced availability. According to the Insurance Information Institute, Georgia ranks low in both homeowners and auto insurance affordability. This is alarming, especially considering that Georgia’s average income is below the national average, making it increasingly difficult for residents to secure affordable coverage. As insurance costs continue to rise, many families find themselves financially strained, struggling to keep up with necessary premiums.

The growing challenges surrounding insurance affordability in Georgia are not solely due to high premiums; they also stem from the frequency of claims and the associated litigation costs. With a significant increase in both auto and homeowners claims, insurers are facing substantial pressure. Consequently, this results in higher premiums for consumers, leaving many to question how they can maintain necessary coverage without incurring financial hardship.

The Impact of Tort Reform on Insurance Costs in Georgia

Tort reform has emerged as a critical topic in discussions about insurance affordability in Georgia. The state’s legal environment has facilitated a surge in litigation, which in turn drives up insurance costs. Analysts estimate that litigation expenses cost Georgia residents approximately $880 million annually, which translates to an average of $1,415 per person. Legislative changes aimed at reforming the tort system could potentially alleviate some of these financial burdens, making insurance more accessible and affordable for residents.

Recent state-level initiatives have highlighted the importance of implementing tort reform to curtail the excessive legal costs that plague the insurance industry in Georgia. By addressing the root causes of inflated litigation costs, lawmakers aim to create a more favorable environment for insurers, which could lead to lower premiums for consumers. Effective tort reform has the potential not only to stabilize insurance costs but also to enhance the overall economic landscape in Georgia.

Rising Litigation Costs and Their Effects on Georgia Residents

The rise in litigation costs has become a significant concern for Georgia residents, particularly in relation to auto insurance. Data indicates that claim frequency, especially for bodily injury and property damage, has surged in recent years. This trend, coupled with a higher rate of attorney involvement in claims, has resulted in increased indemnity payments and rising premiums. As a result, many Georgia residents are grappling with the dual pressures of rising living costs and the need for adequate insurance coverage.

Moreover, the stark reality of the situation is highlighted by the statistics revealing that Georgia’s litigation rates for personal auto claims are nearly three times the median state rate. This alarming trend not only affects insurance affordability but also raises questions about the sustainability of the insurance market in Georgia. As residents confront these challenges, the need for comprehensive reforms becomes increasingly evident.

Climate Risks and Homeowners Insurance in Georgia

Climate change and the frequency of severe weather events are significant factors influencing homeowners insurance in Georgia. With over 134 confirmed disasters leading to losses exceeding $1 billion since 1980, homeowners in vulnerable areas face escalating premium costs. Recent data indicates that many residents in coastal and southern regions may experience double-digit hikes in their insurance premiums or even nonrenewals, highlighting the urgent need for affordable insurance options in the face of climate risks.

As homeowners navigate the complexities of securing adequate coverage, the intersection of climate risk and insurance affordability becomes crucial. Insurers must balance the financial implications of increasing claims due to severe weather with the necessity of providing affordable premiums to residents. This dynamic creates a challenging environment for both insurers and policyholders, prompting discussions about innovative solutions to address these pressing issues.

The Importance of Consumer Awareness in Insurance Affordability

Consumer awareness plays a vital role in understanding the challenges associated with insurance affordability in Georgia. As residents become more informed about the factors that drive up costs, they can better advocate for necessary reforms and make educated decisions regarding their insurance coverage. Organizations like the Insurance Information Institute are dedicated to raising awareness about the implications of rising litigation costs and the importance of tort reform in stabilizing insurance markets.

Additionally, increasing consumer awareness can lead to greater engagement in discussions surrounding insurance policies and potential legislative changes. As stakeholders work together to address the issues of insurance affordability, informed residents can help push for necessary reforms that will ultimately benefit the entire community and enhance the overall stability of the insurance market in Georgia.

Navigating Auto Insurance Affordability in Georgia

Auto insurance affordability in Georgia has significantly declined, with the state now ranking 47th in the nation for personal auto coverage affordability. This downward trend can be attributed to rising claim frequency and increased litigation costs that have plagued the auto insurance market. As a result, many residents are left grappling with high premiums, which can strain their finances and limit their access to necessary coverage.

Moreover, the situation is exacerbated by the high rate of uninsured and underinsured motorists in Georgia, which further complicates the landscape of auto insurance. With insurers facing pressure to cover the rising costs associated with claims and legal fees, many policyholders may find themselves paying more for coverage than they can reasonably afford. Understanding the dynamics of auto insurance affordability is crucial for residents seeking to navigate these challenging waters.

Legislative Changes and Their Potential Impact on Insurance Costs

Recent legislative changes aimed at addressing the rising costs of insurance in Georgia are generating optimism among consumers and industry stakeholders alike. By focusing on tort reform and the need to reduce excessive litigation costs, lawmakers hope to create a more sustainable insurance market that benefits both insurers and policyholders. These changes could help stabilize premiums and ensure that residents maintain access to affordable coverage.

As discussions surrounding insurance reform continue, it is essential for residents to stay informed about potential changes that could impact their insurance costs. Engaging with legislators and advocating for effective reforms can empower consumers and lead to positive outcomes in the insurance landscape. Ultimately, the goal is to foster a more equitable system where insurance affordability is attainable for all Georgia residents.

The Role of Insurers in Addressing Affordability Challenges

Insurers play a pivotal role in addressing the challenges of insurance affordability in Georgia. As the frequency of claims continues to rise, insurers must find ways to manage costs while still providing adequate coverage to policyholders. This balancing act is critical for ensuring that residents can access affordable insurance options without compromising on the quality of coverage.

Moreover, insurers are increasingly looking for innovative solutions to mitigate the impact of rising litigation costs on their operations. By employing risk management strategies and exploring alternative dispute resolution methods, insurers can help reduce the financial burden on consumers. The partnership between insurers and consumers will be essential in navigating the evolving landscape of insurance affordability in Georgia.

Community Engagement and Insurance Affordability Initiatives

Community engagement is crucial in addressing the issue of insurance affordability in Georgia. Local organizations and advocacy groups are increasingly working to raise awareness about the challenges residents face regarding rising insurance costs. By fostering discussions and facilitating educational initiatives, these groups can empower consumers to make informed decisions about their coverage options and advocate for necessary reforms.

Moreover, collaborative efforts between community leaders, insurers, and lawmakers can lead to innovative solutions that address the root causes of insurance affordability challenges. By coming together to share insights and best practices, stakeholders can work towards creating a more sustainable insurance market that benefits all residents of Georgia. Ultimately, community engagement is a powerful tool for driving change and promoting insurance affordability.

Frequently Asked Questions

What factors are contributing to insurance costs in Georgia?

Insurance costs in Georgia are influenced by several factors, including rising claim frequency, increasing litigation costs, and severe weather events. The state’s below-average income levels compared to high insurance expenditures further exacerbate the affordability issues for residents.

How does tort reform impact insurance affordability in Georgia?

Tort reform aims to address excessive legal costs that contribute to rising insurance premiums in Georgia. By reducing litigation costs, tort reform could help enhance the affordability and availability of insurance for residents, particularly in the auto and homeowners insurance markets.

Why is homeowners insurance so expensive in Georgia?

Homeowners insurance in Georgia is costly due to high exposure to climate-related disasters, increasing litigation costs, and the state’s ranking of 42nd in affordability. These factors drive up premiums, making it difficult for residents to find affordable coverage.

What is the current state of auto insurance affordability in Georgia?

Auto insurance affordability in Georgia has declined, with the state ranking 47th in the nation for personal auto insurance affordability. This drop is attributed to rising claim frequency, higher litigation costs, and a significant number of uninsured and underinsured drivers.

How do litigation costs affect Georgia’s insurance market?

Litigation costs have a pronounced effect on Georgia’s insurance market, contributing to increased claims and premiums. The state’s litigation rate for personal auto claims is nearly three times the national median, driving up costs for insurers and, consequently, policyholders.

What challenges do homeowners face regarding insurance in Georgia’s coastal regions?

Homeowners in Georgia’s coastal regions face significant challenges, including potential double-digit premium hikes and nonrenewals due to their vulnerability to climate risks. These factors are compounded by increasing litigation costs and claim frequency, contributing to affordability issues.

What is the significance of underinsured motorists in Georgia?

The rate of underinsured motorists in Georgia is twice the national average, which raises concerns about liability coverage and the overall affordability of auto insurance. This situation can lead to increased costs for insured drivers who may face higher premiums to cover potential claims.

How have legal claims influenced insurance payouts in Georgia?

In Georgia, legal claims significantly influence insurance payouts, as attorney-involved claims dominate personal auto claims for bodily injury. In 2023, these claims accounted for 62% of total claims and 86% of indemnity paid, highlighting the impact of litigation on overall insurance costs.

What measures are being taken to improve insurance affordability in Georgia?

Recently introduced tort reform legislation aims to stabilize insurance costs in Georgia by addressing excessive litigation expenses. This could potentially lead to lower premiums and improved affordability for both auto and homeowners insurance.

How does Georgia’s insurance affordability compare nationally?

Georgia ranks poorly on the national scale for insurance affordability, coming in at 42nd for homeowners insurance and 47th for personal auto insurance. This low ranking is attributed to a combination of high insurance costs, rising litigation expenses, and below-average income levels for residents.

| Key Point | Details |

|---|---|

| Decrease in Insurance Affordability | Insurance affordability in Georgia is declining due to rising claim frequency and insurer costs. |

| Homeowners Insurance Ranking | Georgia ranks 42nd for affordable homeowners insurance. |

| Personal Auto Insurance Ranking | Georgia ranks 47th for personal auto insurance affordability, a drop from 27th in 2006. |

| Impact of Litigation Costs | Skyrocketing litigation costs are affecting insurance coverage affordability and availability. |

| Tort Reform Discussion | Legislative solutions, like tort reform, are being considered to reduce excessive legal costs. |

| Weather/Climate Risks | Georgia has faced 134 weather/climate disaster events since 1980, impacting insurance rates. |

| Claim Trends | Claims and litigation in personal auto lines are increasing, with bodily injury claims 60% higher than the national average. |

| Advertising by Law Firms | Law firms spent $160 million on advertising, with a 119% increase in outdoor ads for lawsuits. |

| Tort Reform Legislation | Recent tort reform legislation may help stabilize rising insurance costs. |

Summary

Georgia insurance affordability is under significant pressure as litigation costs and claim frequency continue to rise. The latest reports indicate that residents face mounting challenges in securing affordable homeowners and personal auto insurance, ranking among the lowest in the nation. With ongoing discussions around tort reform, there is hope for legislative action to alleviate these financial burdens and improve the insurance landscape for Georgians.