Personal Auto Insurance: Key Insights for 2023

Personal auto insurance plays a crucial role in safeguarding drivers and their vehicles while contributing significantly to the U.S. property and casualty insurance landscape. Recent analyses indicate that improvements in personal auto insurance results have propelled the insurance industry to its second-highest net underwriting gain in over two decades. With a remarkable decline in the combined ratio from 102.2 to approximately 94.0, insurers are witnessing enhanced profitability amidst challenging market conditions. These shifts reflect broader insurance industry trends, especially as the sector navigates the impacts of catastrophes and fluctuating loss ratios. As the market responds to these dynamics, understanding personal auto insurance becomes essential for both consumers and industry stakeholders alike.

When discussing personal vehicle coverage, it’s important to consider its overarching impact on the insurance landscape. Terms like auto liability coverage and motor vehicle insurance encompass the essential protection offered to individuals against potential losses stemming from accidents. Recent statistics reveal a notable enhancement in auto insurance performance, driven by favorable underwriting conditions and a marked decrease in the combined ratio. The current state of the insurance industry illustrates how external factors, including catastrophe impacts, can influence the profitability of personal auto insurance. As we explore this critical sector, it’s vital to remain aware of the evolving trends and challenges that shape the future of vehicle protection.

The Impact of Personal Auto Insurance on the Property and Casualty Industry

Personal auto insurance has emerged as a vital component driving the success of the U.S. property and casualty insurance industry. Recent analyses have demonstrated significant improvements in personal auto insurance performance, which have contributed to the industry’s remarkable net underwriting gains. With a combined ratio that has notably decreased from 102.2 to about 94.0, it is clear that effective underwriting strategies and pricing adjustments have positively influenced profitability. This shift not only highlights the resilience of personal auto insurance in a challenging market but also reinforces its critical role in bolstering overall industry performance.

As the insurance landscape continues to evolve, the trends within personal auto insurance are closely monitored by industry experts. The current hard market, characterized by rising premiums and stricter underwriting guidelines, signifies a response to the increased frequency of severe accidents and the associated costs. Insurers are now focusing on enhancing their risk assessment processes to mitigate losses, which is crucial for sustaining profitability in the long run. The interplay between personal auto insurance and broader property and casualty challenges illustrates the need for adaptive strategies that can withstand market fluctuations and evolving consumer behaviors.

Understanding the Combined Ratio and Its Significance in the Insurance Industry

The combined ratio is a key metric used to assess the financial health of insurance companies, particularly in the realm of personal auto insurance. A combined ratio under 100 indicates profitability, while a ratio above 100 signifies losses. Recent reports indicate that the industry’s combined ratio has improved significantly, dropping to approximately 94.0, which is a strong indicator of enhanced underwriting profitability. This improvement can be attributed to a combination of factors, including robust premium growth and a moderate increase in incurred losses, which reflects a more favorable underwriting environment.

Understanding the dynamics of the combined ratio is essential for stakeholders within the insurance industry. It not only provides insight into the operational efficiency of insurers but also highlights the effectiveness of their risk management strategies. As the insurance industry adapts to new challenges, including the impacts of catastrophes and changing consumer behaviors, monitoring the combined ratio will be crucial for evaluating ongoing performance trends. The recent improvements in personal auto insurance further exemplify the positive trajectory that can be achieved through diligent underwriting practices and strategic pricing.

Current Trends in the Personal Auto Insurance Market

The personal auto insurance market is currently experiencing significant changes, driven by various factors including increased driving activity and heightened risk from severe accidents. As the number of drivers on the road has returned to pre-pandemic levels, the frequency of collisions and associated claims has surged. This trend has prompted insurers to re-evaluate their risk exposure and adjust their pricing accordingly, leading to the hardest pricing environment seen in nearly five decades. Insurers are now compelled to adopt more conservative underwriting practices to safeguard their financial stability.

In addition to the uptick in accidents, the personal auto insurance market must contend with the broader economic challenges posed by inflation. Rising material and labor costs have further exacerbated the financial strain on insurers, contributing to an environment where premiums must increase to offset losses. The trends observed in recent quarters reflect a complex interplay of market dynamics, necessitating that both policyholders and insurers remain vigilant. As the market evolves, stakeholders must stay informed about emerging trends to navigate the challenges effectively.

The Role of Catastrophe Activity in Insurance Performance

Catastrophe activity plays a significant role in shaping the performance of the insurance industry, particularly within personal auto insurance. The recent mild catastrophe activity has been a boon for insurers, contributing to the favorable underwriting results seen in the first quarter. Compared to previous years, when severe weather events wreaked havoc on claims and losses, the current environment provides a much-needed respite for insurers. However, the forecast for an ‘extremely active’ Atlantic hurricane season in 2024 serves as a reminder that the threat of catastrophes remains ever-present.

Insurers must remain proactive in their approach to catastrophe risk management to mitigate potential losses. This includes refining their pricing models and enhancing their underwriting criteria to account for the likelihood of catastrophic events. As the industry grapples with the reality of climate change and its impact on weather patterns, the importance of effective catastrophe planning becomes increasingly critical. By understanding the implications of catastrophe activity, insurers can better position themselves to navigate future challenges and sustain profitability.

Navigating Legal Challenges in Personal Auto Insurance Claims

The landscape of personal auto insurance is increasingly complicated by legal challenges that arise from claims disputes. As the number of accidents and severe injuries rises, so does the involvement of attorneys representing claimants. This trend has led to a surge in legal costs and claims litigation, further straining the resources of insurance companies. Insurers are now faced with the dual challenge of managing claims while also contending with potential legal abuses that may arise from the current environment.

To effectively navigate these legal challenges, insurers must adopt comprehensive strategies that encompass both claims management and legal risk mitigation. This includes investing in legal expertise and employing data-driven approaches to assess the validity of claims. By enhancing their claims processes and fostering transparency, insurers can minimize disputes and improve customer satisfaction. As the personal auto insurance market continues to adapt to these legal complexities, a proactive stance will be essential for maintaining both profitability and trust among policyholders.

The Influence of Inflation on Auto Insurance Pricing

Inflation is a significant factor influencing the pricing dynamics of personal auto insurance. As the costs of materials and labor rise, insurers are compelled to adjust their premiums to maintain profitability. The current inflationary environment has heightened the urgency for insurers to carefully analyze their underwriting practices and pricing strategies. This not only affects the bottom line for insurers but also impacts policyholders who may face increased premium costs as a result.

In response to inflationary pressures, many insurers are exploring innovative pricing models that reflect the true cost of coverage while remaining competitive in the marketplace. This may include the adoption of technology-driven solutions that improve risk assessment and underwriting efficiency. By embracing these changes, insurers can better manage the challenges posed by inflation and ensure that they continue to meet the needs of their customers. The interplay between inflation and auto insurance pricing will be a critical area to monitor as the industry adapts to changing economic conditions.

Future Outlook for Personal Auto Insurance

The future outlook for personal auto insurance is shaped by a variety of factors, including economic conditions, technological advancements, and evolving consumer preferences. As insurers continue to navigate the complexities of the market, maintaining a focus on innovation and adaptability will be essential for long-term success. The recent improvements in underwriting results signal a positive trend, but the industry must remain vigilant in addressing emerging risks and challenges.

Looking ahead, the integration of technology into underwriting and claims processes will likely play a pivotal role in shaping the future of personal auto insurance. From telematics and data analytics to artificial intelligence, these tools can enhance risk assessment and improve operational efficiency. As the industry embraces digital transformation, insurers must also prioritize customer engagement and education to foster trust and loyalty. By proactively addressing the needs and concerns of policyholders, the personal auto insurance sector can ensure a sustainable and prosperous future.

The Importance of Risk Assessment in Personal Auto Insurance

Risk assessment is a cornerstone of personal auto insurance, as it directly influences underwriting decisions and premium pricing. Insurers must thoroughly evaluate the risk profiles of individual drivers to ensure that they are accurately pricing coverage based on potential loss exposures. The current environment, characterized by increased accident rates and legal complexities, has heightened the importance of effective risk assessment practices. By leveraging advanced data analytics and risk modeling, insurers can make informed decisions that align with their profitability goals.

In addition to traditional risk factors, insurers must also consider external influences such as economic conditions and regulatory changes that may impact their risk exposure. As the personal auto insurance market evolves, staying ahead of these trends will be crucial for insurers seeking to maintain a competitive edge. Continuous refinement of risk assessment methodologies will enable insurers to adapt to changing circumstances and ensure that they are adequately prepared to address emerging challenges and opportunities in the marketplace.

Consumer Behavior and Its Impact on Auto Insurance

Consumer behavior plays a pivotal role in shaping the dynamics of the personal auto insurance market. As drivers become more aware of their coverage options and the implications of their driving habits, insurers must adapt their offerings to meet these evolving preferences. The rise of technology and digital platforms has empowered consumers to compare policies and seek out the best value, leading insurers to enhance their customer engagement strategies. Understanding consumer behavior is essential for insurers striving to remain competitive in an increasingly crowded marketplace.

Moreover, the growing trend of telematics in auto insurance is transforming the way insurers assess risk and set premiums. By utilizing data from connected devices, insurers can gain deeper insights into driving behaviors and adjust premiums accordingly. This not only rewards safe driving practices but also fosters a more personalized insurance experience for consumers. As the industry continues to navigate shifts in consumer expectations, embracing innovative approaches to engagement and risk assessment will be key to achieving long-term success.

Frequently Asked Questions

What is personal auto insurance and why is it important?

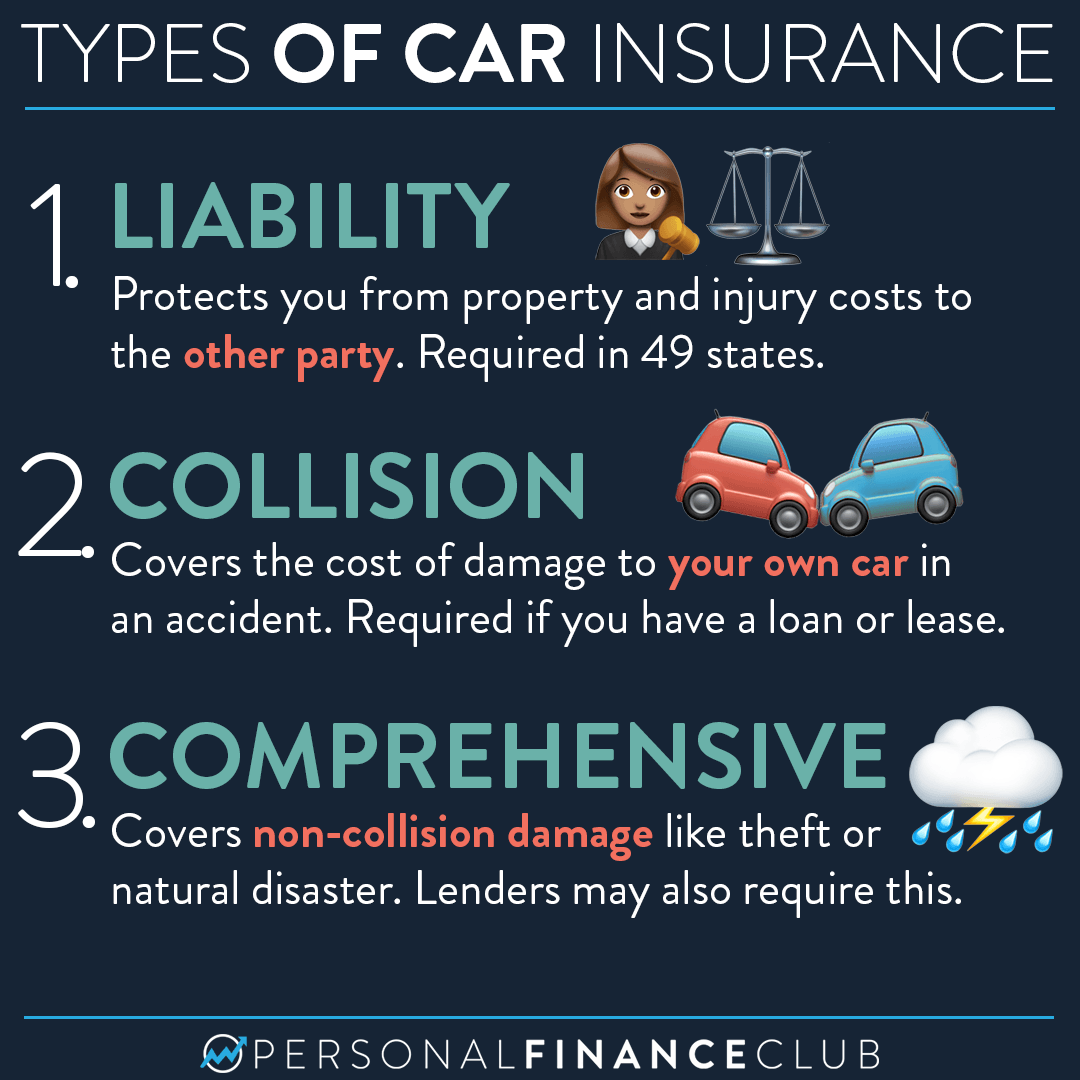

Personal auto insurance is a policy that provides financial protection against physical damage and bodily injury resulting from traffic collisions, as well as liability that could arise from incidents involving your vehicle. It’s essential because it helps cover repair costs, medical expenses, and legal fees, ensuring that drivers can manage unforeseen events without severe financial burden.

How does the combined ratio affect personal auto insurance premiums?

The combined ratio is a key indicator of an insurance company’s profitability, representing the ratio of incurred losses and expenses to earned premiums. A combined ratio below 100 indicates profitability, which can lead to more stable personal auto insurance premiums. When the combined ratio is high, insurers may increase rates to maintain profitability, impacting policyholders.

What trends are currently shaping the personal auto insurance market?

Current trends in the personal auto insurance market include rising premiums due to increased claims from severe accidents and higher repair costs driven by inflation. Additionally, the market is experiencing the hardest pricing environment in 47 years, as insurers adjust rates to align with the rising costs of providing coverage.

How do catastrophes impact personal auto insurance claims?

Catastrophes can significantly affect personal auto insurance claims, as severe weather events lead to increased vehicle damage and higher claim payouts. Although recent data shows mild catastrophe activity has benefited the industry, forecasted severe weather patterns could lead to increased losses and potentially higher premiums for policyholders.

What is the significance of the direct incurred loss ratio in personal auto insurance?

The direct incurred loss ratio measures the percentage of premiums used to pay for claims. In personal auto insurance, a lower loss ratio, such as the reported 66.7%, indicates better underwriting performance, which can result in lower premiums and improved profitability for insurers. This ratio is crucial for assessing how effectively an insurer is managing its claims costs.

Why are personal auto insurance rates increasing in 2023?

Rates for personal auto insurance are increasing in 2023 due to several factors, including the rise in accident severity, increased repair costs, and legal expenses related to claims. Additionally, the industry is navigating a challenging hard market that has led to stricter underwriting practices and higher premiums to ensure financial stability and cover rising losses.

How can policyholders navigate the current hard market for personal auto insurance?

Policyholders can navigate the current hard market for personal auto insurance by shopping around for competitive rates, considering higher deductibles to lower premiums, and maintaining a clean driving record. It’s also beneficial to review policy coverage regularly to ensure it meets current needs while managing costs effectively.

What can we expect for personal auto insurance in the upcoming years?

In the upcoming years, personal auto insurance may continue to see fluctuations in rates due to ongoing challenges in the insurance industry, such as inflation, severe weather patterns, and changing driver behavior. Insurers will likely adapt their pricing and underwriting strategies based on market conditions, which could affect policyholder premiums and coverage options.

| Key Points | Details |

|---|---|

| Improvement in Results | The personal auto insurance sector contributed to the U.S. property and casualty insurance industry’s second-highest net underwriting gain since 2000. |

| Combined Ratio | The combined ratio improved from 102.2 to approximately 94.0, indicating profitability. |

| Loss Ratio | A direct incurred loss ratio of 66.7% in the personal auto sector suggests an estimated combined ratio of 95.6. |

| Current Trends | The personal auto insurance market is experiencing the hardest pricing environment in 47 years. |

| Impact of Catastrophes | Mild catastrophe activity in the first quarter aided the strong results. |

| Future Concerns | The ongoing high inflation and rising accident rates may challenge future profitability. |

| Market Stability | Insurers’ performance and driver rates are expected to take time to stabilize. |

Summary

Personal auto insurance has shown remarkable improvements in recent quarters, contributing significantly to the profitability of the U.S. property and casualty insurance industry. With the combined ratio dropping to approximately 94.0, the sector indicates a positive trend toward profitability, despite facing challenges such as high inflation and increased accident rates. As the market continues to evolve, it is crucial for policyholders and industry stakeholders to remain vigilant and adaptable to ensure the long-term stability of personal auto insurance.